How Do Lenders Assess Investment Loans

Banks have tightened up on investment loans in 2019, and with all the different lending options that are still available to a multitude of different investors, it’s really important to understand, the differences between different banks and products and how they affect your portfolio on an ongoing basis.

Watch this video to understand how banks assess investment loans in 2019 and what you need to consider when applying for an investment loan in 2019.

Property Investment Market 2019

Buying land or a house or any piece of real estate is often considered one of the better financial decisions that one can take. Real estate investments not only have considerable long-term value, but they can also offer passive income options which grow exponentially over time. This is true irrespective of the price fluctuations which take place in the market.

For example, currently there’s been a slight decrease in the property prices lately, however, if you take into consideration market history and growth patterns over time, you’ll notice that there’s growth in valuation to be seen even in times of lowered property prices.

Purchasing real estate, irrespective of whether it’s for investment purposes or home ownership, is not quite that easy. Since no one has an exorbitant amount of cash just lying around, ready to buy a property on the fly, most owners have to apply for and get a home investment loan approved before they can move forth with their investments. And investment loans aren’t exactly handed out to everybody.

Investment applications are carefully examined, scrutinized and assessed by lenders (which in most cases are banks) before they are approved, and the loans are granted.

This raises the two fundamental questions:

- How do banks assess investment loans for approval purposes?

- How does one decide which lender to go to when in the market for an investment loan?

Read on to find out how these two questions can influence your application.

Things to Consider When Applying For an Investment Loan

When it comes to investment loans, most people don’t take into consideration the many factors which banks or lenders use to evaluate their applications.

Try to put yourself in the credit assessors’ shoes and think about how banks assess investment loans. Most people are often only interested in inquiring about how to get an investment loan, in short, which bank to approach. You should know that while the latter is equally important to consider, it is the former which needs to be prioritized first.

For approval purposes, here’s how banks assess investment loans:

Loan To Value Ratio (LVR) – The Key To Your Interest Rate

If you ask a bank: how do lenders assess your investment loan, one of the top factors listed will include LVR. LVR, or Loan to Value Ratio, is necessarily the amount of your loan as compared to the total value of your property. It primarily represents the amount that you’re borrowing from the bank, which is represented as the percentage value of the piece of real estate you already own (or is being used as security for the loan).

To calculate LVR, a bank divides the amount of the loan by the total value of the real estate. The greater the LVR, the greater is the risk to the bank or lender, and thus, this changes and limits the types of products available.

In some cases we have seen interest rates based on different tiers of the LVR that is 50%, 60%, or 80% and above.

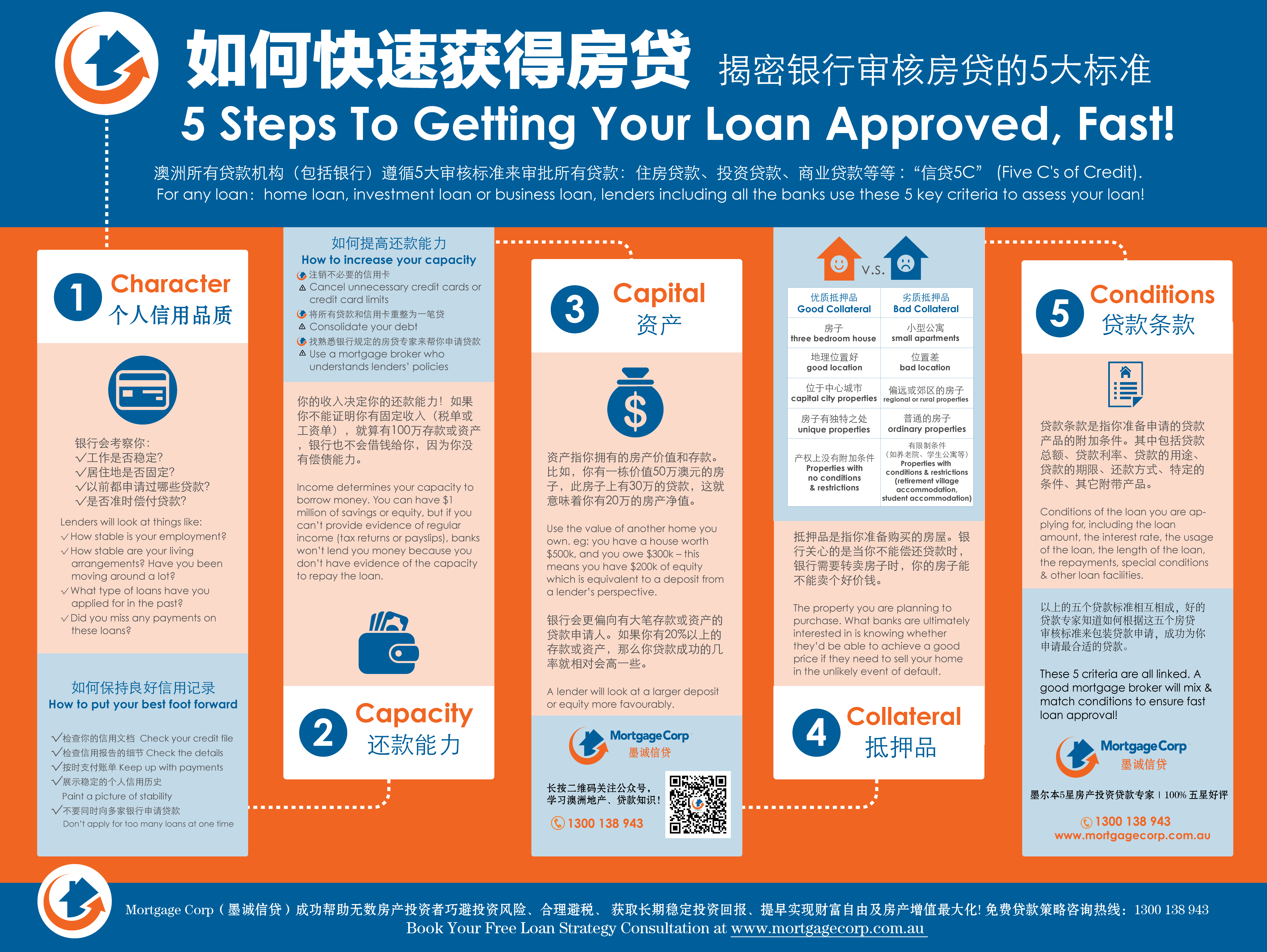

The 5 Key Criteria Banks Use to Assess All Mortgages

If you want to learn how to get an investment loan for sure, on your first application, make sure you know all about the Five C’s of Credit. This is a very elaborate system devised to help lenders gauge a client’s credit worthiness in order to get a rough estimate of the possibility of a default by a borrower. The Five C’s include character, collateral, capacity, capital, conditions.

Character – Your reputation

This is the borrower’s (your) credit history. It’s mainly your reputation with the bank and other creditors, such as utilities, credit card, other loans or services in which you have established by your record of paying back your debts. Each borrower has credit reports maintained by the credit bureaus of a country. This report outlines all the information necessary to calculate a credit score. Think of it as a cover letter of sorts for your investment resume, after all, it is the very first thing a lender will look at in order to evaluate your investment loan request.

Capacity – Your capacity to repay the mortgage

The capacity is essentially the measure of a buyer’s ability to repay the loan they’re taking. It uses the client’s income, job, and job stability, comparing it against the total amount of debt to assess the borrower’s financial standing.

Most investors are under the impression that it’s the existing assets that bankers first take into account when assessing an investment loan, but it’s actually the net income that is evaluated first.

Capital – Your savings or equity

This refers to any monetary contribution the buyer has made towards their investment, for example, a possible deposit or your equity. While a deposit may be the down-payment you’ve made towards acquiring your new property, the equity refers to the existing value of any other property which you may own.

The capital can often shifts the decision of the lender against you – especially in case you don’t have enough. The capital indicates your loyalty towards returning the bank’s money. The lesser the capital, the greater the chance of you defaulting on your loan, and the lesser your chances are for loan approval.

Collateral – Security

This is the assurance offered to the lender that you can pay off the loans in time. If you are unable to follow through, the lender can repossess the collateral to recover their investment. Think of it as a guarantee or security offered to the banks that you’ll be timely with your payment, just because you have something to lose.

Conditions – The Conditions of the Loan

The conditions lay out the details for the lender about how the borrower intends to utilize the loan and for how long. They don’t necessarily have anything to do with you as an applicant for a loan, but rather they’re more concerned with the factors directly influencing the loan itself that you have applied for.

The usual conditions are the amount of principal, interest rate, and the lender’s choice of financing a particular buyer’s investment loan.. This is mostly for assurance purposes to ensure that the money is being used towards the intended objective.

Video: How to Get Your Loan Approved, Fast

Watch the video below where our loan strategist Neil Carstairs explain what these 5 criteria are and how do lenders assess your loan based on these 5 criteria.

Other Factors Lenders Consider When Assessing Investment Loans

Rental Income

When considering an investment property for a standard rental agreement, appraisal from an agent would generally suffice. However, if the client is looking at different types of incomes from the property i.e. boarding, serviced apartments or AirBnB’s, then different policies will come into play. In such cases, some lenders may not even use or accept this as a form of investment income. As such, it affects a buyers borrowing capacity, directly influencing the amount they can borrow.

Moreover, different lenders use different percentages of the income – this means some lenders will use 80 percent, or even 75 percent only, thus changing the borrowing amounts yet again.

Cross Securitisation or Split Facilities

Cross-collateralisation, or cross securitisation, is a specific investment strategy which refers to borrowers using more than one single property as security to acquire an investment loan. This is mostly bundling your loans together and lowering your LVR.

Split Facilities is where we access equity from property and arrange a separate loan on the new purchase not connected to the original property purchase. It is a ‘standalone’ product. This means if you sell or refinance each loan, they remain independent of each other.

When lenders assess your investment loan, they take into account cross securitization when approving or rejecting an application.

Negative Gearing

The concept of negative gearing is applied when a potential buyer borrows money to invest, but at the end of the financial year, has the interest and running costs collectively add up to become more than what their investment income is. This effectively has them running at a loss. A borrower can use this net loss in order to claim a tax deduction against their other incomes.

This factors into investment loans because not every lender takes into account negative gearing benefits for loan approval.

Assessment Rates – RBA Cash Rates + Buffer

Every lender in Australia has a standardised variable interest rate as per the interest rate policy. Using the cash rate policy of the Reserve Bank of Australia, the bank calculates a base interest rate which applies to all of their borrowers. However, when lenders assess your home and investment loan, they don’t determine a buyer’s capacity on the base interest rate.

Rather, they normally add an extra 2% or 3 percent points or what is called a ‘buffer’ to the official Standard Variable Rates during their calculations. This added percentage is a bank’s cushion. It is their way of mitigating risk in case the standard variable rate was to suddenly fluctuate. This is also their way of covering their funding costs as well as their profit margin per application. The combined rate, used as a buffer, is a bank’s assessment rate.

These ‘buffers’ can be applied to other loans not being refinanced, or to the loans taken from other lenders. Irrespective, these buffers can and do affect your borrowing capacity.

Loan Terms – The Length of Your Loan

If you’re wondering how to get an investment loan for certain, think about the loan term before you apply for one. That is because this is one of the factors that lenders seriously take into account before accepting or rejecting an application. A loan term is essentially the duration of time the loan lasts. If the overall period is quite long, a lender automatically assumes that due to the minimal monthly payable, there are fewer chances of complete investment recovery – mostly due to the high probability of a borrower’s circumstances changing over time.

As with the majority of the investment options, it seems to be more favorable to take an interest only approach if you have your own home loan, too. Most lenders offer terms ranging from one to ten years, which then converts to principal and interest. The longer the interest-only term, the higher the payments will be when it converts into principal and interest.

However, while a shorter loan term does translate into a higher monthly payment for the borrower, it means greater security for the bank, thus effectively increasing the chances for an investment loan approval.

Serviceability – Ability to Repay

One of the last, but by no means the least, important factors are taken into account when lenders assess your investment loan is serviceability. Simply put, a borrower’s serviceability is their ability to meet all the requirements of loan repayment. By factoring into the equation the potential buyer’s income, their credit history, their current commitment and expenses, amount of loan, and percentage required, a lender calculates whether or not, you, as a borrower, will be able to make returns on their investments in a timely, profitable manner.

Now that we’ve effectively explained to you some of the major factors which influence a lender’s loan assessment and approval decisions, let’s get back to the second of the two questions we raised at the beginning of this article i.e.

Which Lender To Choose For Your Investment Loan?

This is where Mortgage Corp comes in.

As your property investment mortgage specialists, we help professional and aspiring investors build and grow their portfolio, including carefully selecting lender of choice in order to improve their chances of investment loan approval.

Loan specialists at Mortgage Corp keep up to date with our lender current loan products, policies and requirements, as they change on a regular basis. Based on these shifting policies and the current client scenario and financial portfolio, we help clients choose a most suitable lender and loan product.

Your next step to getting the right loan & loan structure for long term investment success

Your next step to getting the right loan & loan structure for long term investment success

There’s no doubt that analysing the many factors that go into a loan can be confusing and time-consuming. At Mortgage Corp, we take the time to understand your goals and unique situation and then come up with a mortgage strategy. We are committed to not only getting you the right loan but more importantly, getting you the right loan structure for long term investment success. Our strategic approach means we take a long-term view, aimed at maximising future investment options so you can build a successful property portfolio faster… and reach your financial freedom sooner.

Book A Free Loan Strategy Session

About Neil Carstairs

Neil is the founder of Mortgage Corp, an active property investor and awarding winning MFAA accredited finance broker with more than 10 years’ mortgage broking experience. Currently, Neil is one of only few MFAA Certified Mentors in VIC/TAS region.

He is known for his strategic approach to investing and ability to reach fast, successful outcomes for clients where his industry peers could not. Connect with Neil on LinkedIn.

The Mortgage Corp Difference

Based in Wantirna South, Melbourne (opposite the Westfield Knox Shopping Centre), Mortgage Corp is the most loved mortgage broking firm in Melbourne with consistent 5 star customer reviews. Mortgage Corp specialises in helping successful professionals and property investors maximise their return and strategically structure your loan for long term investment success.

Unlike most mortgage brokers that may be able to help you with general loans but simply don’t have the skills, experience or resources to genuinely help home buyers and property investors maximise long-term wealth, Mortgage Corp take a long-term, strategic approach to help our clients maximise their overall investment result. Request a Free Loan Strategy Session with our senior mortgage strategist Neil Carstairs today!