First Time Investor Buys First Investment Property with Loan Guarantor

Family Pledge Loan Case Study | Mortgage Corp

Clients at a glance

Executive Summary

Mortgage Corp helped a first time investor secure her first investment property using a family guarantor. This young professional had a limited deposit and had just changed her job, but Mortgage Corp was able to refinance her parents’ home loan and help her buy an investment property, which allowed the entire family to save approx $9,000 in Lenders’ Mortgage Insurance (LMI) as well as the parents saving approx $300/month on interest.

Overview

Client: Amy and her parents, new clients of Mortgage Corp 2016 after reading Mortgage Corp reviews on Google

Marital status: Single, living at home with parents

Income: $80,000

Occupation: physiotherapist in a private practice

Suburb of parents’ home: Mount Waverley, VIC 3149

Suburb of investment property: Mount Waverley, VIC 3149

Objective: family wanted to help their daughter buy her first investment property to set her up for her future

Results: bought first investment property through a family guarantor and reduced interest rates on parents’ loan by approx. $3600 per year

Background

Amy was a young professional, working in private practice as a physiotherapist. She was living at home with her parents in Mount Waverley when she came to see us.

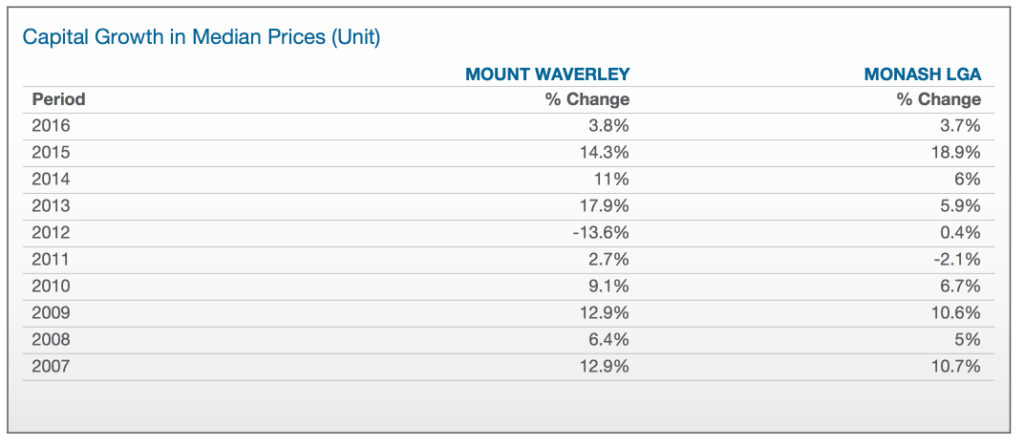

She was keen to purchase an investment property, also in Mount Waverley, a decision which her parents also supported. The family felt that Mount Waverley would be a good area to invest in, as over the last few years it was a well sought after area for many high income and overseas buyers, with median capital growth by an astonishing 33% in 2015 (compared to a decline of -1.2% in 2012).

We’ve also heard great things about the area as many of our clients in Mount Waverley have been able to capitalise on the growth in their equity and downsize for a solid retirement plan or use their equity to help their children buy their first homes. Some of these families have seen profits exceed $1 million and the area has also started to see a lot of interest from developers in particular, town houses.

Amy had had a few years experience in her field however had just changed jobs and was about to start at her new place in a few weeks’ time. She also had a limited deposit and enquired whether she would be able to obtain financing for an investment property.

Sources: RP Data 2017

The Challenges

When Amy came to see us she had just finished at her previous position and was about to start her new job. We told her that it was probably not the best time for her to apply for a loan as banks would want to see at least one or two payslips, along with a letter from her employer explaining her employment conditions.

Also, whilst Amy had saved up a good deposit from working for the last few years and living at home, based on the price of the properties she was interested in, she would still be up for thousands of dollars in lenders mortgage insurance.

Objectives

- purchase an investment property in Mount Waverley

- pay $0 lenders’ mortgage insurance (LMI)

The Solution

Amy thought she might have to wait 3 or 4 months before she could get the necessary information (eg: payslips etc.) to apply for a loan. However we knew of a couple of lenders that would allow us to only provide one payslip for her conditional loan application, based on the fact that she was employed on a full time basis. This meant we could get the process moving quicker so she could buy her investment property sooner.

To get around the problem of her limited deposit, her parents offered her a family guarantee on their property. This allowed her to use some of her parents’ equity to help her buy a property so she wouldn’t have to pay lenders’ mortgage insurance.

Her parents currently had a $1.2 million home loan with one of the major banks. Whilst we could have gone through the same bank as her parents for Amy’s loan of $420,000, we were able to find a better deal with another major bank that would allow:

- Amy’s parents to save money due to a more competitive interest rate than their current bank – they ended up saving approx. $3600 a year in interest

- Amy to use the family guarantee to avoid paying lenders’ mortgage insurance

- Amy to have a more competitive interest rate on her loan as well

Amy’s parents were happy for us to refinance their loan to help their daughter. However before we were able to do that, we had to show the new bank that there was an appropriate exit strategy for them given they were both over 55 years of age. For example, banks are not keen to extend a new 30 year term loan if it means the borrowers would be 85 years of age by the end of the loan term. We had to show that they could repay their loan before reaching retirement in order to have the refinancing approved.

It worked out that their home’s value was quite high (approx. 1.7million) and they also had two other investment properties that were of great value that were entirely paid off. If they sold those properties and dipped into their super, they would be able to pay off their entire home loan of $1.2million. This meant that they didn’t have to apply for a shorter loan term – which would have made repayments very high – and we were therefore able to save them thousands in interest per year under the refinanced loan.

Results

- Amy bought an investment property in Mount Waverley, soon after changing jobs

- Avoided lenders’ mortgage insurance through the family guarantee

- The entire family saved thousands in interest from the refinancing

Note: for privacy reasons, names used in this case study are not real client names.

For real Mortgage Corp customer reviews, visit

mortcorpdev.mortgagecorp.com.au/testimonials/ or

www.facebook.com/pg/mortgagecorp/reviews/

What’s Next?

Keep reading No Deposit Family Guarantee Home Loan or Request A Free Loan Strategy Session